RKLB: T - 1

"T‑1" is rocket countdown speak for "we're 1 second from launch". For a stock, one year is close.

In 2022, I wanted exposure to the space economy. SpaceX was the obvious choice, but private. I tried to buy through an SPV (Special Purpose Vehicle) that turned out to be a scam, a story for another day. Meanwhile, Elon's attention started splintering across politics and Twitter, making me nervous about concentration risk in anything he touches.

So I went looking for alternatives. That's when I found Rocket Lab.

What struck me wasn't ambition; everyone in space has ambition. What struck me was the execution. Electron already had a proven track record: 24 successful launches under its belt. Reliable tech. Its management had made a smart choice: don't compete with SpaceX head-on. Pick a niche and dominate it.

I started buying at $4- $5 to test the water. The stock went sideways. In 2023, I sold for NVIDIA, and figured Rocket Lab needed more time to mature. But I kept watching. In late 2024, I started gradually buying again at $8 after earnings beats. In 2025, RKLB launched 21 times, beating their own target of 20 launches.

So here’s my current take: Rocket Lab is one big step away from being a space juggernaut instead of a niche “small-launch company.”

That step is Neutron.

This is a "worse is better" bet.

The Neutron Advantage

What excites me about Neutron isn't that it's revolutionary.

It's that it’s optimized.

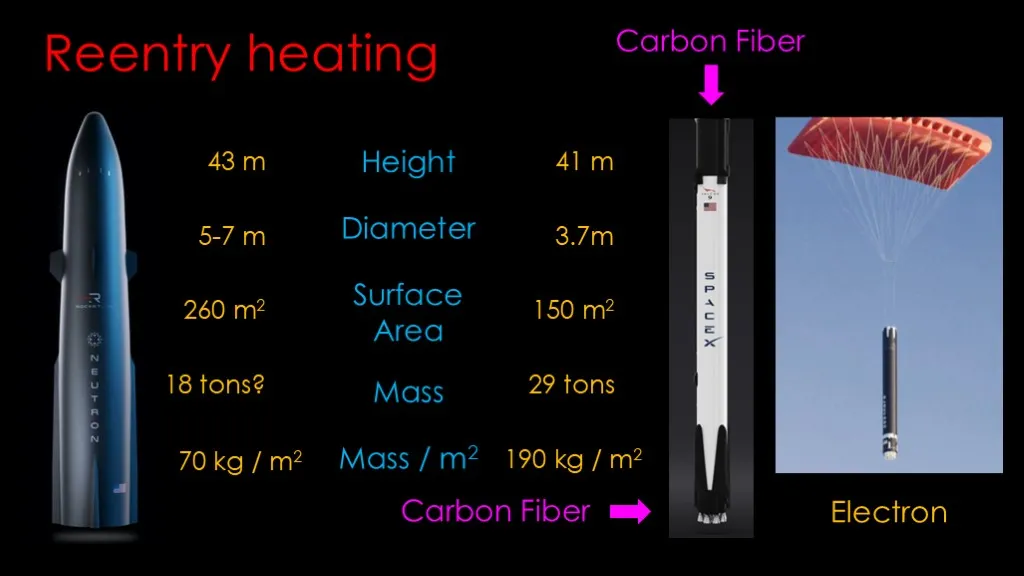

Falcon 9 is a mature, battle‑tested medium‑lift workhorse, arguably the best value rocket ever fielded. However, it’s also a design that started from a disposable architecture. Neutron, by contrast, is a clean‑sheet medium‑lift rocket designed from the start around partial reusability and operational simplicity.

Here is what’s different:

- Lighter launch infrastructure and marine recovery assets, because the rocket is lighter and smaller.

- Fairing attached to the first stage, no recovery cost for fairing.

- Carbon fiber construction → better strength-to-weight

- Wider, chunkier first stage that decelerates naturally, potentially without reentry burn.

- The second stage is suspended inside the fairing rather than supported from below, and is not subject to aerodynamic forces during ascent. The end result is a lighter second stage that costs less.

- Archimedes engine runs at low chamber pressure, leaving room for growth as the program matures.

- Methalox fuel burns cleaner, making engine refurbishment easier than Falcon 9’s Kerolox, enabling higher cadence.

The entire launch and recovery process is simpler. A smaller rocket means a higher flight rate. A higher flight rate means better amortized costs and lower insurance.

Currently, almost all other medium-lift rockets in development, Chinese or American, are basically Falcon 9 knockoffs. Neutron is an actual upgrade, Falcon 9 2.0, designed while SpaceX pours resources into Starship.

RKLB proved execution with Electron. I think Neutron will likely follow.

The bet

If Neutron reaches orbit and the reuse/refurb workflow is genuinely simpler, Rocket Lab can compete on cost and cadence in a segment that’s growing fast.

The Competition

Falcon 9: the benchmark

Falcon 9 is mature, reliable, and heavily optimized. Any “Neutron upside” has to be measured against the fact that Falcon 9 already exists, already works, and already flies a lot. Initial unit economics don’t have to match Falcon 9’s, but I want to see decreasing cost and increasing margin similar to Electron.

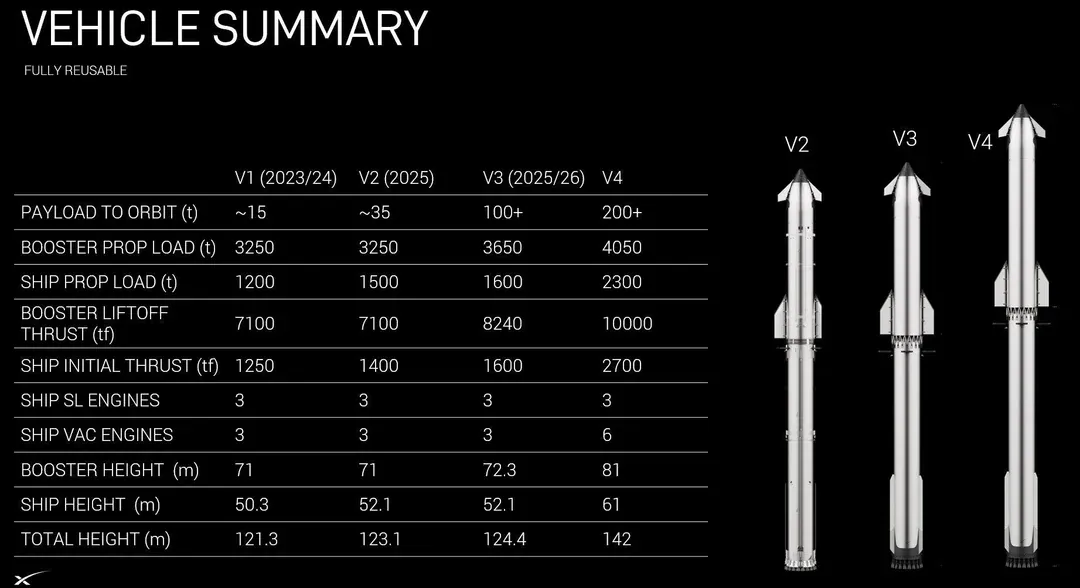

Starship: the wild card

Starship could eventually reset the cost curve for very heavy lift. But it comes with genuine uncertainties that matter for near‑term commercial markets:

- Payload integration and mission diversity are still evolving. Publicly, Starship has been focused on Starlink‑style deployment concepts so far; broader commercial payload workflows and a mature “catalog” of mission profiles take time to develop.

- Demonstration vs operations. It’s one thing to fly test articles; it’s another to deliver routine, insured commercial payloads on a predictable schedule.

- In‑orbit refueling and complex architectures. Those unlock the grand vision, but they add novel failure modes, and nobody gets that right instantly.

Gwynne Shotwell (SpaceX COO) has publicly indicated that Falcon 9 will be around for years during the transition. Even in a “Starship succeeds” world, Falcon 9 can remain a major workhorse longer than people expect, and Neutron’s window could be competing in the shadow of Falcon 9 rather than competing after Falcon 9 disappears.

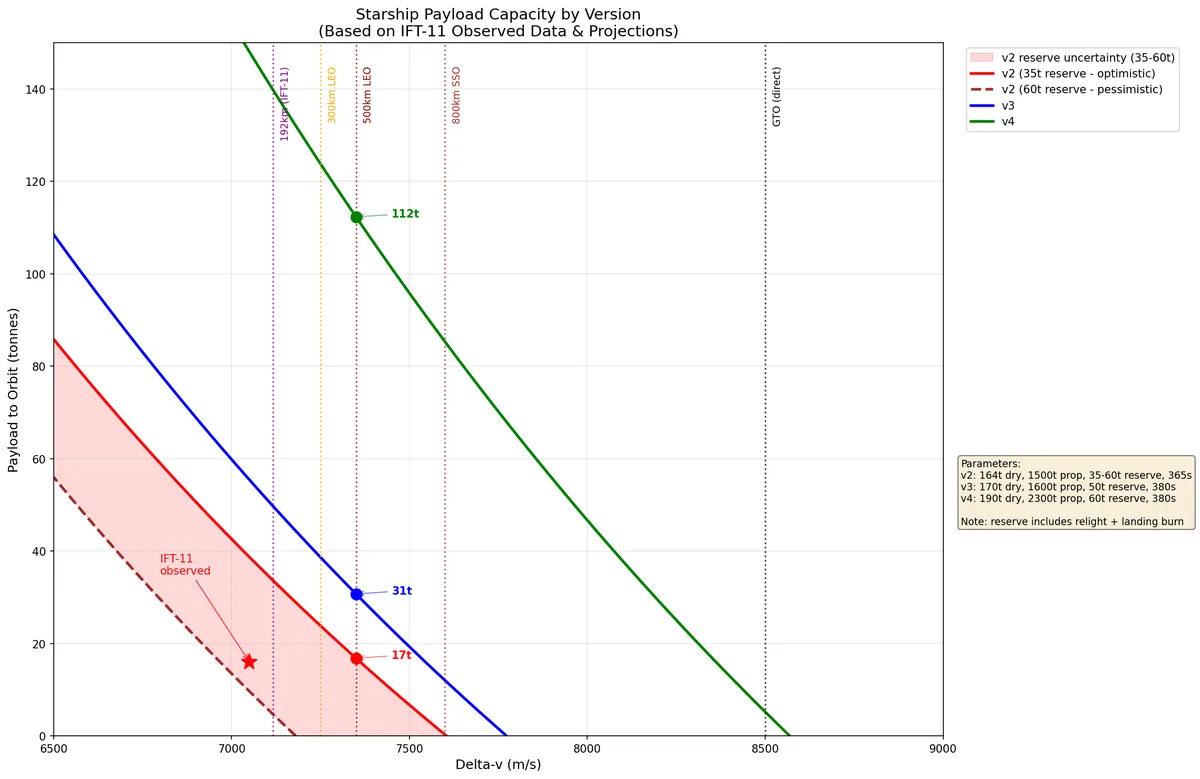

I also ran some numbers using Starship's IFT-11 telemetry. The result suggests the gap between SpaceX's published specs and operational reality is significant. The first two versions of Starships would have a hard time reaching orbit based on the inferred performance. See detailed analysis in the appendix.

New Glenn: capability isn’t cadence

Blue Origin has the resources to brute‑force progress, but the biggest open question is cadence.

Yes, Amazon could funnel Kuiper launches into Blue Origin and bootstrap volume. But if the economics don’t work, that becomes a governance problem, not just an engineering problem.

New Glenn might also find a strong niche in government and deep‑space missions. That’s valuable. The unanswered part is whether it becomes a high‑cadence commercial platform.

China: likely soon, but geopolitics matters

China will likely achieve reusability in the next few years. But due to geopolitics, western customer likely wouldn’t touch them.

The Launch Vehicle Landscape

Here’s the mental model I use:

- Electron = taxi

- Neutron = van

- Falcon 9 = small bus

- Starship / New Glenn = double-decker bus

Yes, bigger vehicles can offer a lower cost per kilogram if you can fill them and if the mission profile fits. But many satellite operators don’t want a double-decker. They want a taxi or a van: a specific orbit, a specific schedule, and fewer compromises.

That flexibility is what customers pay for, and Rocket Lab’s launch pricing trend suggests the market has been willing to pay a premium for it.

Evidence: Electron unit economics trend

Below is a rough “implied average” based on segment revenue, cost of revenue, and completed Electron missions. It’s not perfect, since revenue recognition and mix effects can distort any single year/quarter, but directionally it shows pricing power and improving cost efficiency.

| Year | Electron missions completed | Launch Services revenue ($M) | Launch Services cost of revenue ($M) | Implied avg price / launch ($M) | Implied avg cost / launch ($M) | Sources |

|---|---|---|---|---|---|---|

| 2020 | 7 | 33.085 | 45.87 | 4.73 | 6.55 | Rocket Lab 2022 10-K |

| 2021 | 6 | 38.971 | 53.82 | 6.50 | 8.97 | Rocket Lab 2022 10-K |

| 2022 | 9 | 60.686 | 67.64 | 6.74 | 7.52 | Rocket Lab 2022 10-K |

| 2023 | 10 | 71.900 | 63.80 | 7.19 | 6.38 | Rocket Lab 2024 10-K |

| 2024 | 16 | 125.400 | 90.80 | 7.84 | 5.68 | Rocket Lab 2024 10-K |

| 2025 (first 9 months) | 14 | 123.200 | 78.00 | 8.80 | 5.57 | Rocket Lab 10-Q (Q3 2025) |

Market Demand

My primary reason that very heavy-lift vehicles would not pose a threat to Neutron is the demand for them.

Falcon Heavy can launch >40 tons to LEO in reusable mode, yet flies far less frequently than Falcon 9. That's a market signal. Big rockets are incredible tools, but not every mission needs one, and not every market can fill them at high cadence.

Here's the thing: satellites don't all want the same orbit. Different inclinations, different altitudes, different RAAN (the orientation of the orbital plane). And changing orbits is expensive. Playing Kerbal Space Program (a rocket simulation game) taught me that an orbital plane change can cost more delta-V (think mileage of a car) than getting to orbit in the first place.

So the hub-and-spoke model for launch, pack a giant rocket, deploy to one orbit, let satellites maneuver to their final destinations, forces each satellite to carry extra propellant and complexity. That's mass that could have been payload. Point-to-point means the rocket takes you directly where you need to go.

This maps to the Boeing vs Airbus bet in the 2000s. Airbus built the A380 superjumbo for hub-and-spoke operations, with passengers connecting through mega-hubs. Boeing built the 787 for point-to-point, direct flights between city pairs. Boeing won decisively. Airbus discontinued the A380 in 2021. And the penalty for an airport layover is just a few hours. The penalty for an orbital "layover" is satellite mass and lifespan.

An optimized medium-lift rocket might actually be the sweet spot.

Worst Case

NSSL (National Security Space Launch) does not want a monopoly. Governments don’t like single points of failure, whether technical, geopolitical, or corporate.

If you assume the market wants multiple providers at the high end, then the current three credible players:

- SpaceX

- Rocket Lab

- Blue Origin

are likely to survive.

Worst case for Rocket Lab: Starship eventually works extremely well, and Neutron becomes the default “second option” because customers and governments still don’t want single‑provider dependency.

That’s not a terrible worst case.

A Note on Satellites

One thing many people miss: Rocket Lab’s spacecraft/satellite systems business is not “a side hustle.” It generates meaningful revenue from components, solar, reaction wheels, separation systems, and complete spacecraft capabilities.

I’m not leaning on it for the main upside case. To me, launch drives the narrative and the optionality. But the space systems segment matters because it:

- diversifies revenue,

- builds customer relationships upstream of launch,

- and gives Rocket Lab a way to compound even when launch is lumpy.

If Neutron succeeds, the space system is a bonus. If Neutron fails, space systems aren’t likely to yield asymmetric returns.

What I’m watching next

Over the next 12–24 months, here’s what matters to me:

- Neutron milestones: hardware readiness, pad readiness, and a credible first‑flight window. I expect the first flight by the end of 2026.

- Archimedes maturity: test cadence, demonstrated stability, signs of refurb friendliness.

- Contract quality: not just headlines—quantity, cadence expectations, and pricing.

- Operational proof: any signal that reuse/refurb is trending toward repeatability.

- Margins/backlog: whether it compounds while Neutron ramps.

What would change my mind

I’m wrong if:

- Neutron slips repeatedly or experiences multiple failures.

- Reuse becomes technically possible but operationally expensive (slow turnaround, high inspection burden).

- Rocket Lab can’t reach sufficient cadence.

- The business requires sustained dilution at a pace that overwhelms execution gains (a “finance problem” rather than an engineering problem).

RKLB: T - 1

Rocket Lab is one step away from becoming a major player in the medium-lift market. Electron proved they can execute. Neutron is the next test.

I don't have the same decade of conviction I built with NVIDIA. I'm not a rocket scientist. But I see a company that picks achievable targets and hits them, run by a CEO who stays focused while competitors chase grandiose visions.

Sometimes, the taxi company and the van company thrive while everyone else fights over who builds the biggest double-decker.

Sometimes, worse is better.

Appendix

Starship

The current design can only launch Starlink due to its tiny payload door. It would need a redesign for other commercial satellites. It still hasn't delivered anything to orbit. Development feels slow. In-orbit refueling needs time to work out the bugs since nobody has done it before. I'm skeptical they hit that timeline. We already have Starship V1 and V2, neither of which has reached orbit. What I suspect, based on Eager’s analysis and my own, is that the payload to LEO (Low Earth Orbit) might be much smaller than the initial design, which makes it economically unviable. Hence, SpaceX keeps increasing the size of the rocket.

The Raptor engines are also running at unprecedented chamber pressure (350 bar, ~3x that of the BE-4, Merlin 1D, or Archimedes). Might this cause more fatigue failures? With these extreme specifications, I won’t be surprised if there are more delays, like Tesla's HW5 or the ATI R600 series.

Starship Payload Analysis

Telemetry data from Starship Flight 11:

- MECO at ~1300m/s ground speed.

- The apogee is 192km@~7720m/s inertial speed.

- 360s second stage burn + 5s relight + 15s landing burn.

- 16 tons payload.

Using the idealized rocket equation. The back-computed inert mass (Starship + reserve propellant) for orbit insertion: 200-225 tons. The implied LEO payload is much less than the 35 tons advertised by SpaceX.

It also illustrated why SpaceX is trying to remove as much heatshield as possible, lower Starship's weight, and push engine pressure to unprecedented levels. The payload capacity drops quite quickly as a function of delta-v for a full reusable Starship.

Glossary:

- Delta V: think of this as the mileage of your car

- Isp: specific impulse of an engine, unit is seconds—think of this as the fuel economy of an engine