NVDA: Two Decades of AI

In September 2015, I sold all my NVIDIA shares and made about $450.

Earlier that month, the Fed had said something to the effect that it would raise rates in the near future, and I got spooked. It was potentially the first rate hike since the 08 recession. I'd held the shares for two months. I was a new investor, an intern, and I had no idea what I was doing. So I did what felt safe: locked in my profit, sold everything, and went for lunch.

NVDA was around $22 when I sold. Today it's around $190, after a 4:1 and a 10:1 split, so roughly 300x.

That $450 profit turns out to be one expensive lesson I've learned. Those shares would be worth $900K+ today. I wasn’t wrong about NVIDIA. I was right, but I couldn't hold on at the time.

I’ve since held through multiple 50% drawdowns without flinching. Turns out, being right isn’t the hard part.

Seed

I first got to know NVIDIA in 5th grade, when I was trying to build a gaming PC. My knowledge came from MicroComputer, a Chinese hardware magazine. The big story that year was the transition from DirectX 9 to DirectX 10 and the adoption of the associated unified shader architecture.

Two giants were fighting it out: NVIDIA and ATI (later acquired by AMD). They picked opposite approaches. NVIDIA bet on a cleaner, more generalizable design: the shaders work on a single operation at a time. ATI, on the other hand, went for something complex: its shaders can work on five independent operations simultaneously. On the surface, ATI’s solution seems more efficient, but when the dust settled, NVIDIA's G80 architecture won by a wide margin, because it is hard for the compiler to pack 5 instructions together every time. ATI's R600 architecture struggled with delays and performance per watt. It was released almost a year late, yet it still can’t match NVIDIA’s flagship 8800 GTX. And since then, at least to me, ATI/AMD has never recovered in the high-end GPU market. The top-performing GPU for gaming has always been Team Green.1

But what stuck with me more wasn't graphics.

The magazine talked about GPGPU—General-Purpose GPU, where various scientific workloads leverage GPU’s massive parallel compute capability, for example, fluid dynamics, protein folding, etc. Also, an upcoming SDK called CUDA that would let programmers control the GPU using a C/C++ like language.

This was years before "AI accelerator" became a thing. NVIDIA was already telling developers: This isn't a graphics card. It's a new kind of computer.

There was also this co-processor2 framing I still remember:

As Moore's Law slows, computing shifts toward co-processors. Intel was trying to make GPUs into CPU co-processors. NVIDIA was trying to make CPUs into GPU co-processors.

We now know how that ended.

That was the first seed: NVIDIA wasn't just a gaming company. The more generalized approach from NVIDIA aged better and set them up for what came after.

I didn’t know it yet, but I was building the first layer of a mental model I’d eventually have to trust.

Thesis

Fast forward to 2013. I was preparing my application to UW's CS (Computer Science) program, thinking about what I want to work on. I start researching why we don't have capable AI yet; why we can't just simulate a bunch of neurons, which we know quite a bit about, and get at least some basic intelligence.

That curiosity pulled me into the early modern deep learning3 era.

The first story that caught my attention was Google Brain's famous "autoencoder learns a cat" moment. Researchers discovered that if you scale neural nets and data enough, they start to learn high-level concepts without hand-designing everything. That was a different world from the older AI that felt brittle and rule-based.

I also watched Geoff Hinton's talks: one at Google, one at UBC. In the UBC talk, there are two notable sections: First, a breakthrough in image recognition. AlexNet won the ImageNet 2012 by a wide margin. And it did it using two NVIDIA GTX 580s. The second, perhaps more significant now, is Ilya Sutskever's work on language models using recurrent neural networks. The results were hilarious. One of the examples in the slides: “The meaning of life is the tradition of the ancient human reproduction: it is less favorable to the good boy for when to remove her bigger.” Clearly gibberish, maybe some sense, but not quite. But what is clear is that it requires significantly less human design. In case you don’t know, Ilya was the chief scientist and co-founder of OpenAI.

At that point, the logic felt inevitable:

- Deep neural net scales.

- Scaling needs compute.

- Compute means accelerators.

- Accelerators mean NVIDIA GPUs with CUDA.

CUDA becoming the default compute language didn't surprise me. After all, it was years in the making. But it did make me excited as an aspiring CS major. It felt like we might finally get computers to do something genuinely intelligent, not just if-else their way through the world.

Buy

After my first internship at Amazon in 2014, I opened my first brokerage account with TD Ameritrade (A lot of paperwork for an international student). I thought about buying NVDA, but looking at the stock chart, GPU computing was nowhere to be found, much to my dismay. Maybe GPU computing isn’t what I was hoping for. I bought TSLA and MSFT instead as my first test of the market. Sold TSLA at a loss in early 2015, MSFT at a small profit. Net loss overall.

However, by mid-2015, the thesis had become impossible to ignore.

In research labs where I worked, neural nets meant NVIDIA GPUs. The state of the art kept advancing. GoogleNet had reached human-level image recognition. The best object detection work used deep learning. And it wasn’t just in the lab; industry adoption was also quickly picking up.

That summer, I started my Google internship. With the lump sum bonus in hand, I bought 130 shares of NVDA at $19.53 per share pre-split.

My thesis wasn't complicated:

- Researchers training deep neural nets/deep learning use NVIDIA GPUs almost exclusively.

- Deep learning is dominating vision and speech.

- Deep learning scales with compute and data better than other approaches.

- It's moving into real products.

What I also learned is that search and ads still use human rules and linear models for the most part, and are trained on CPUs. And I thought deep learning has a long way to go. The runway is loooong.

Then, one morning, when I was just starting my workday, checking my brokerage account, NVDA suddenly jumped to $25. Turned out NVIDIA beat its earnings by a large margin. But I wasn't fully confident. Data center revenue was still tiny compared to gaming. The DC growth rate wasn’t stellar either.

Then September came, and the headlines were all about rate hikes, and NVDA declined for several days, dropping to around $22. Fearing I would lose all my profits, I sold everything.

There wasn’t a particular rationale for me to sell everything. That was me getting spooked by macro noise.

I'd done the work. I understood the technology. I had a view that the market hadn't priced in. Yet, I gave it all up because the stock dropped for a few days.

The irony is that I knew the thesis was intact. Nothing about CUDA or deep learning had changed. But I didn't have the conviction to trust my own analysis over the headlines and price movements.

Rigid rules

I was very lucky to start full-time at Amazon Lab126 in a computer vision team in February 2016. Training neural nets still meant NVIDIA GPUs. But I didn't buy back in immediately.

Two reasons. First, I'd learned some "responsible" personal finance: emergency fund, 401k, IRA, then invest. Second, I anchored hard. I wanted to buy back below $30, near where I'd sold last year. And to no one’s surprise, that never happened.

NVDA didn't wait for my checklist; it just kept climbing. By the time I started dollar cost averaging into the stock in December 2016, the stock had already gone up to around $110. I followed the textbook: emergency fund, max out retirement accounts, then invest. The stock didn't wait. I missed a 4x run.

I had discipline now. But discipline isn’t conviction; conviction has to be earned through time.

Validation

Then 2017 happened.

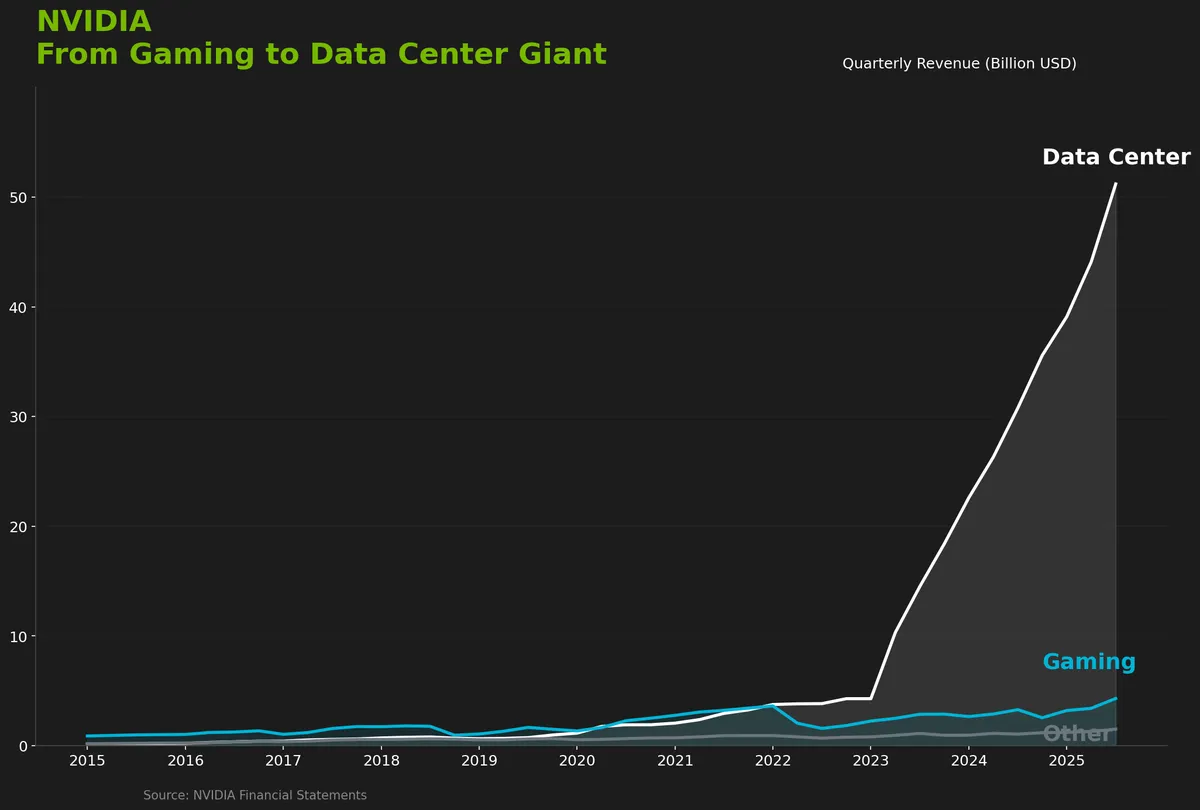

NVDA surged. Data center revenue grew faster than gaming. CUDA adoption accelerated, not just in research, but in production systems. Gross margin also expanded, and the software moat started showing up in pricing power. This was the inflection.

For the first time, I wasn't just hoping my thesis was right. I was watching it become a reality. The model I'd built in my head: NVIDIA as a platform company, CUDA as a 10-year bet on accelerated compute. It was generating predictions that were coming true. That's when NVDA became my conviction.

Hold

By summer 2018, NVDA had run high, hitting around $280, partly on crypto mania. Then everything hit at once: crypto unwinding, trade war, and rate hikes.

This time, I have learned my lesson and didn't flinch. I held and kept buying.

My framework had matured:

Data center should eventually dominate. Gaming could be cyclical, and crypto distorted it. Data center GPUs, however, are productive capex. They generate returns for the buyer. In my mind, it was only a matter of time before DC revenue became the center of gravity. As Jensen said it best: “The more you buy, the more you save.”

NVIDIA is software + hardware. Wall Street often treated NVDA like a chipmaker, with zero analysts mentioning CUDA in the news. I saw it as a platform company. The deepest moat wasn't the silicon; it was CUDA, the tooling, and the developer ecosystem. That's not something a competitor can replicate in a few years.

One obvious competitive threat was custom silicon, and it remains so to this day. Google had TPUs, Amazon had Inferentia, and Microsoft was using FPGAs (at the time). Custom silicon, specifically designed for AI, will be more cost-effective. I have two rebuttals:

- NVIDIA's moat isn't the hardware. It's the garden around it. Even for the most mature, ASIC, namely TPU, developer support outside Google is still subpar. If I were to start an AI company, I'd pick NVIDIA GPU every time, because engineering time matters more than the theoretical FLOPS/dollar.

- ASICs are married to a specific workload mix. If operations shift, specialized hardware looks worse. GPUs remained the best programming abstraction for evolving workloads. And because ASICs are focused on a narrow set of workloads, they benefit less from economies of scale.

Between 2021 and 2024, I got calls from financial advisors at Wells Fargo and Chase. The message was always the same: you have concentration risk; you should diversify. These were prudent advices. By the numbers, my portfolio was irresponsible. However, their framework and mine were measuring different things. They saw a percentage. I saw a platform moat that wasn't yet priced in.

Meanwhile, on the technology side, language models were crossing a threshold. BERT and early GPT made me feel like NLP (Natural Language Processing) was getting its AlexNet moment, when scaling, architecture, and compute reshape an entire domain. It had done it for speech and vision; it had now come to language. It was computer vision 2012 all over again, except with a much broader addressable market. Text is everywhere, and it touches every product.

NVIDIA wasn’t just a GPU company; it was and still is an accelerated computing platform. And at that layer? Basically a monopoly.

Trim

In December 2022, ChatGPT took the world by storm. It was decades of research and engineering concentrated in a singular product. Google declared a “code red” to catch up. All the tech companies started to hoard GPUs.

Then the numbers became undeniable: data center revenue was through the roof, dwarfing gaming. The thing I'd expected for years was now a reality.

Now that everyone’s eyes are on NVIDIA, things have started to change.

AI became consensus. I have seen more mentions of CUDA in the news lately. When everyone believes the same thing, the market tends to stop paying you for believing it. You can still make money, just not the same asymmetric returns.

Bottlenecks shift at scale. When the AI buildout becomes enormous, GPUs may not be the only constraint. Think memory, power, and fab capacity. When the bottleneck moves, value capture can move too.

At one point, NVDA had become 80% of my portfolio. That concentration might have been fine before. By then, it wasn't right anymore. I rotated capital to places where I saw better risk-adjusted upside. Starting in mid-2024, I began trimming gradually, through early 2025, right before the tariff escalation.

It has exceeded my wildest dreams that NVIDIA has become a 5 trillion dollar company. I would never have imagined such a scenario when I first bought my 130-share stake as a junior college student.

I'm still bullish on accelerated computing. I'm just less bullish that holding on to NVDA will generate outsize returns from here.

That intern who sold at $25 wasn't wrong about NVIDIA. He just didn't yet know how to be right. It took years and a lot of held positions through ugly drawdowns to learn the difference. I don't know if I'll find another NVIDIA. But I know what conviction feels like now: not hope, not stubbornness, but the growing confidence when your model keeps generating correct predictions, which can only be built through time.

My first dedicated GPU was the 8800 GT, using the G92 (an iterative improvement over G80) architecture and produced on TSMC's 65nm node.↩

In 2006, there was a company called Ageia, which was later acquired by NVIDIA. Its hardware and software were used in physics simulations in games. It was folded into the NVIDIA GPU, demonstrating its flexibility.↩

Deep learning can be used interchangeably with neural networks. Some used it to avoid the stigma associated with neural networks during the last AI winter.↩